Where is the recession?

When the Fed started interest rate hikes, my friends in academic economics thought that a recession was a 50-50 proposition; meanwhile, friends in finance considered it a practical certainty. So, I’ll make myself a hostage to fortune, and ask what happened?

Here, I will explore three theories about what may have upset those expectations:

— Credibility. Tyler Cowen recently laid out the case:

“A long-standing tradition in macroeconomics, sometimes called rational expectations, suggests that a truly credible central bank can lower inflation rates without a recession. If the central bank announces a lower inflation target, and most people believe the central bank, wages and prices adjust in rough sync with demand. All nominal variables move upward at a slower pace, markets continue to clear, and the economy keeps chugging along. Because individuals in markets believe the disinflation process is for real, they are willing to act in accordance with it in their pricing and wage-demand decisions.”

In short, the Fed’s action convinced people that the problem would be solved. Then, they adjusted prices accordingly, solving the problem. If that seems circular to you, you understand it correctly.

— The “Real Theory”. What I term “Real Theories” hold that recessions are caused by society redirecting its productive resources, in contrast to theories that center on sticky prices, credit constraints, etc. However, Covid offered just such an opportunity to reallocate labor and change business strategies, pre-empting the rearrangements that would have caused this recession.

— Personal Finances. Due to shelter-in-place orders forcing thrift, a stock market surge, and federal transfers paired with state tax cuts, household balance sheets swelled in the pandemic and its aftermath. That build-up has kept consumption unusually high during the last year and a half, buoying the economy.

So, which of these have evidence to back them?

Why are there recessions?

A recession is a prolonged decrease in economic activity. GDP, the measure of that activity, is generally broken into four categories: consumption, net exports, government spending, and investment. Yet, at least since the fifties, American recessions have really only been slumps in investment. Unsurprisingly, government spending ends up increasing (to fight the recession), and net exports slightly increase a little (as Americans import a little less, but the world continues demanding our exports). Yet surprisingly, consumption barely moves. With the important exceptions of COVID and the GFC, consumption tends to slow its growth or less often slightly decline.

Instead, recessions are really the combination of two dramatic swings: a rapid spike in unemployment and a drop in investment. To me, it is not obvious why this happens. Why should the labor market suddenly unravel? The unemployment rate slowly creeps down. Why does not it slowly creep upwards as well? When it goes up, it only seems to shoot upwards in a recession. I have similar wonders about investment. To take one example, stock prices drop in recessions. In some sense, the stock’s price should be the discounted present value of future profits. A normal recession would diminish those profits for only a few years, a very small chunk of the entire lifetime for the company. The swings in the market make no sense from this perspective. You could argue that many businesses risk going under in recessions, causing risk-averse investors to abjure stocks. However, if that were driving behavior, we would expect the at-risk firms to sag in price but for others to pick up as they proved more resilient than expected. But, that’s not what we see. Furthermore, shouldn’t the market price into every stock the forecast of a recession about once a decade? In which case, only evidence of recessions becoming more frequent should effect stock prices, not the occurrence of an individual recession.

So, why should there be recessions?

The answer taught in school is the standard Keynesian account. In that telling, people begin losing their jobs in some initial shock, and they stop being the consumers that other businesses depend on. Those businesses begin to shed workers in a chain reaction. The reasoning is sound, and no doubt was a major problem in Keynes’ time. However, we have taken Keynes's advice, and developed economies have experimented with programs to compensate the unemployed, to subsidize the employment for those at risk of layoffs, and to otherwise stimulate demand. It seems those efforts have largely succeeded, so with the exceptions of the GFC and COVID, consumption no longer substantially changes during American recessions. Is it really plausible that the persisting small changes in consumption are creating the havoc in labor and investment markets that we still suffer?

While I won’t pretend to have any final answers, these lines of skepticism have pushed me towards “Real Theories” of recession. A “Real Theory” would emphasize changes in the actual process of producing goods/services instead of centering monetary factors or aggregate demand. For reasons of labor law, market power, or psychology, when times are flush managers hate firing people. Meaning that during an expansion, it becomes rare to fire people without cause. That friction means that divisions or businesses with outdated models could persist past their economic viability. Once a recession begins, managers get a green light to make those overdue layoffs and rethink their strategy.

I have not heard a good “Real Theory” that explains recessions’ investment drought. Austrian economics attempts to answer this question by blaming monetary policy. Unnaturally, low-interest rates trick investors across the entire economy into propping up a variety of unsustainable business models. Why those errors are all discovered at the same time seems hard to explain.

With that inconclusive discursion (is there any other kind?), let’s return to whether last year’s recession worries ever had any plausibility.

Did Policy Actually Tighten?

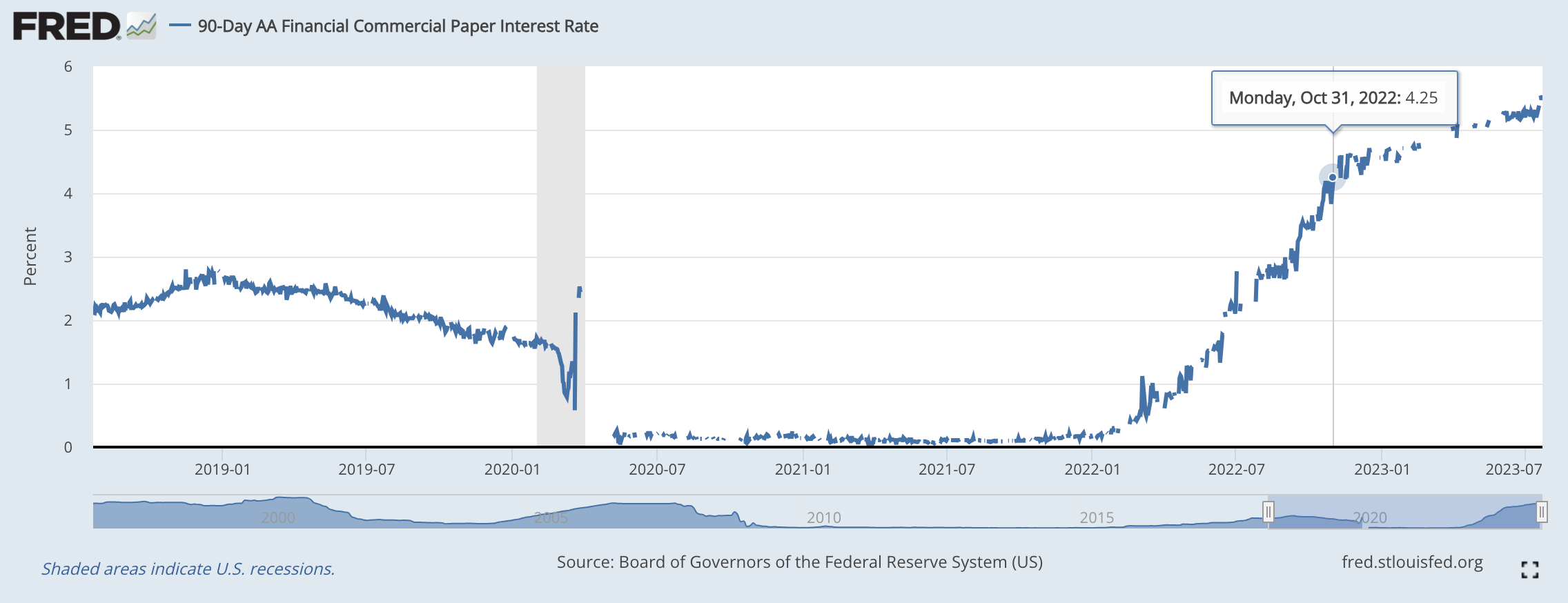

After the Fed’s moves, the average mortgage rate now hovers around 7%, up from 2.75% before. Meanwhile, highly rated-commercial paper now pays 5% instead of its previous rate of near zero. However, the stance of monetary policy is not necessarily more contractionary. That depends on how inflation expectations changed at the same time.

Let's say you lent me $100 on the promise of receiving $105 next year. That would seem a tempting offer. However, if you expect high inflation, 1 dollar of next year’s money might only buy the equivalent of 90 cents in today’s money. The deal no longer looks so good. Therefore, we have to compare the stated increase in interest rates to the market’s change in inflation expectations. If inflation expectations increased more than the Fed hiked, borrowing could have actually gotten cheaper, stimulating the economy not contracting it.

One imperfect proxy for those expectations is the breakevens, the inflation rate implied by comparing inflation-indexed government debt to its vanilla non-inflation-indexed cousin. The one-year breakeven rate hit a maximum of 4.22% in June 2022 and the five-year breakeven topped out at 3.59% in March of that year. So, around a two-point swing from the previous consensus of slightly below 2%. That would indicate that monetary policy has gotten tighter. Nominal rates increased in the 4-5 percent range, and at least as bond traders are concerned, expected inflation only increased 2 points.

However, there’s no easy way to say whether the implied inflation expectations of FT-reading bond traders have any connection to the inflation expectations of a South Dakotan car dealership owner, who has to decide whether to take out a loan for a new location. Uniformity makes modeling easier, but there’s no arbitrage mechanism that imposes uniform views of inflation across the economy. Thus, it’s hard to say whether that car dealership owner has higher or lower expectations than that 2 percent. That matters because whether people taking out business loans perceive borrowing to have gotten cheaper or more expensive in part determines whether the policy will actually be contractionary. Plausibly, someone who has spent their entire career in an era of low inflation is slow to adjust and keeps that model of the world in the back of their mind. If so, their expected inflation would be lower than the bond trader’s, and monetary policy would be even more contractionary than the numbers above suggest. That would be my base case for how the world works.

On the other hand, there’s ample evidence of political partisanship becoming a driving force in how consumers and business owners answer surveys of economic mood. Imagine a Fox-viewing South Dakotan car dealership owner thinking inflation will stay really bad. According to neo-classical economics, high expected inflation would increase the attractiveness of borrowing (a chunk of your debt would be inflated away so why not borrow more), and he would become more likely to engage in economic activity today. However, according to the emotional logic of mood affiliation, inflation being here to stay is bad for the economic climate, so investing in that new dealership location would be risky. All of which is to say, outside of finance, people’s notion of expected inflation is likely incredibly hazy, and as nominal rates rose, I would bet the average participant in the economy considered it more expensive to borrow compared to last year, not minding expected inflation.

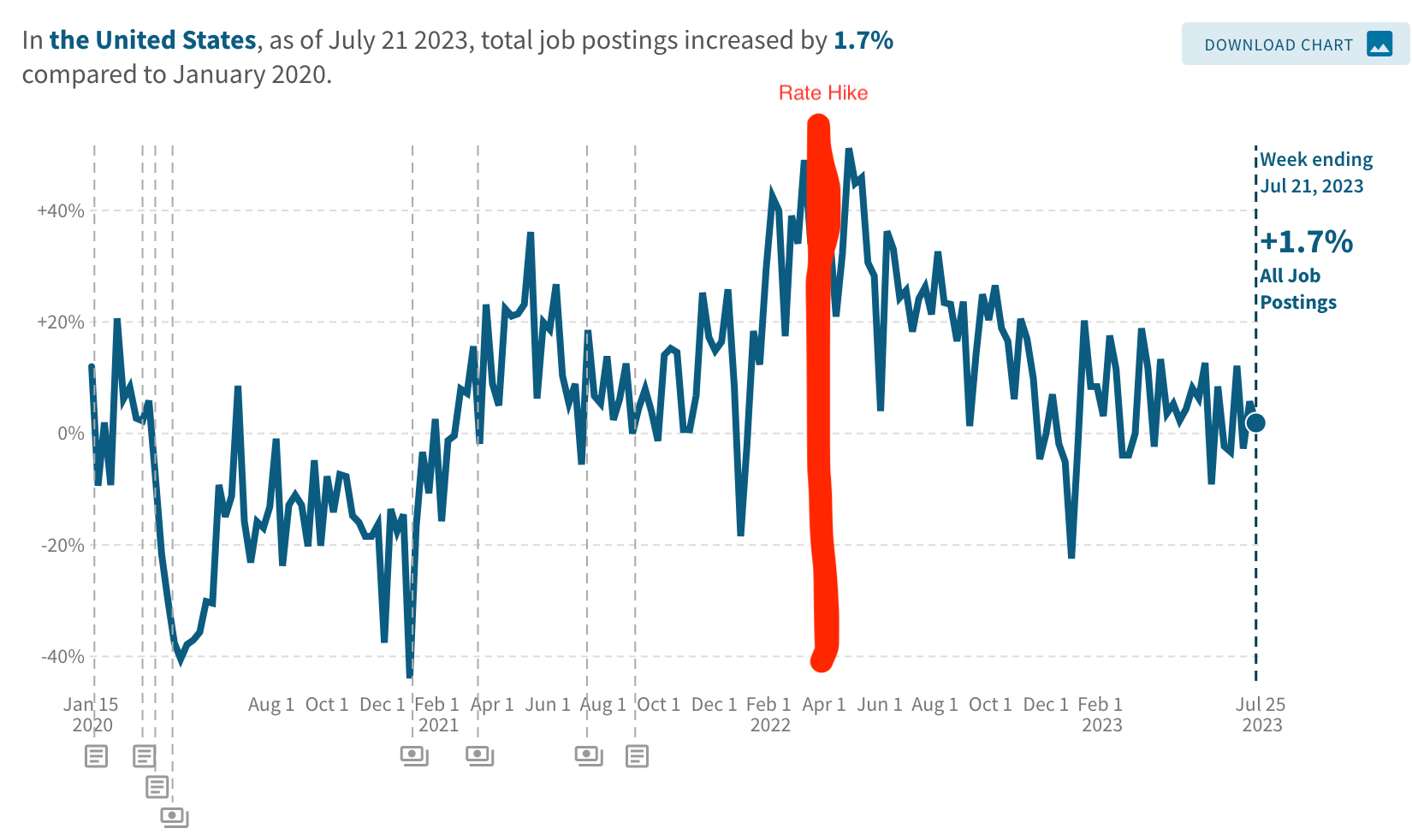

The labor market offered further evidence that policy was contractionary. Below is a graph of all new job postings from Raj Chetty’s Opportunity Insights. The first Fed rate hike was in March 2022, and a month later the job market began cooling. Monetary policy is thought to work with lags, so a response that fast makes the timing of the events seem coincidental. On the other hand, we would expect a country with a more developed financial system to transmit the effects of monetary policy more quickly. Thus, the contemporary United States might have a faster reaction time than a meta-analysis looking back in time and across countries might estimate. If I had to wager, I would guess that this was not a coincidence:

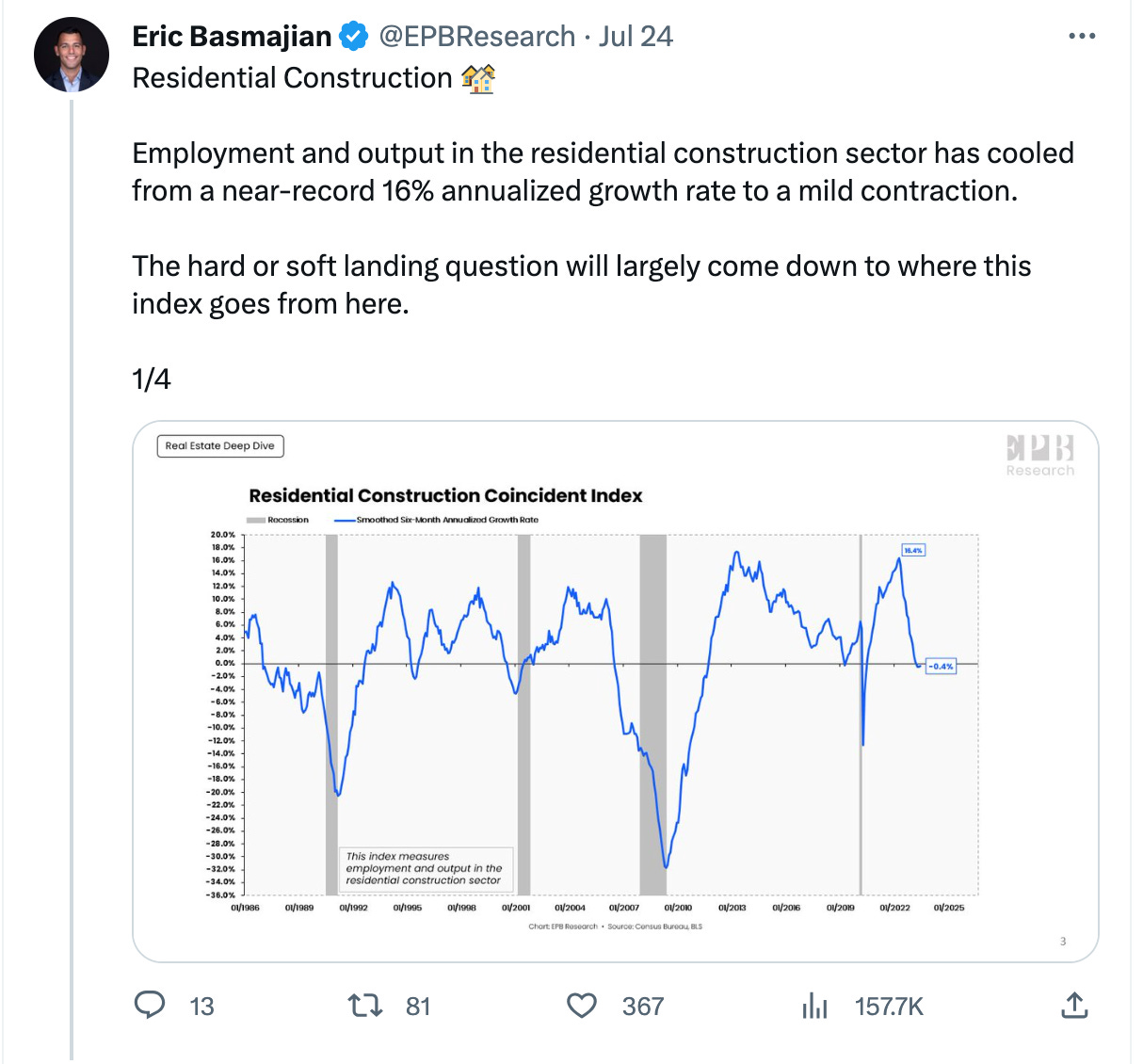

Certainly, in tech hiring and residential construction, the effects of monetary policy were almost immediate. Supporting the idea, that lags might be short in the contemporary US economy. In the graph below, residential construction started dropping right after the rate hike.

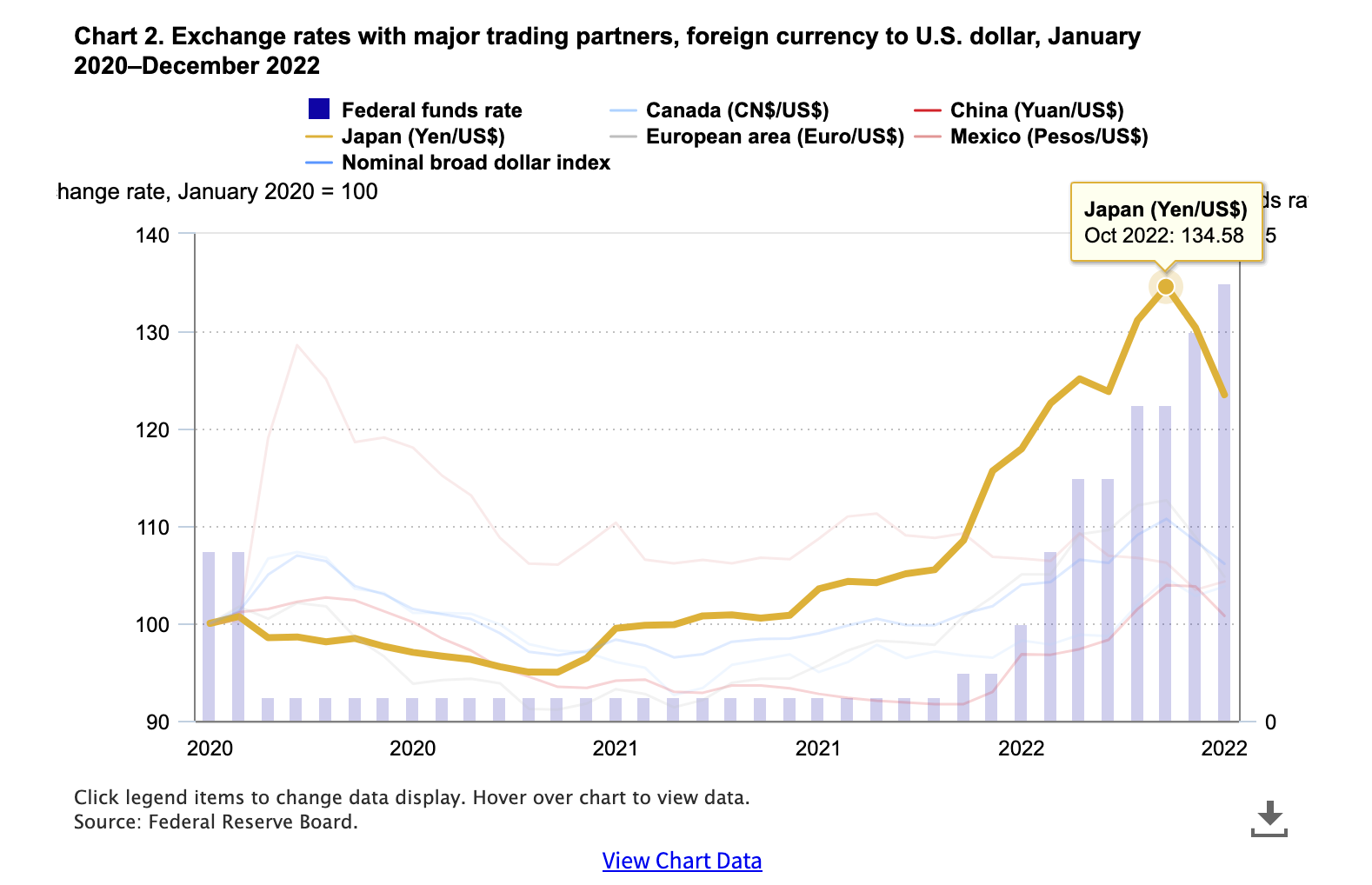

In further evidence of tightening, the dollar appreciated indicating that investors certainly felt that real interest rates increased. (Only if they perceived higher US interest would they have bought more US assets, driving up the dollar’s price). Thus, with the caveat that there is no one expected inflation rate, overall it seems like policy tightened moderately.

Monetary Policy Channels

Generally, the channels of monetary policy can be lumped into three buckets: investment, wealth, and exchange rates. The investment story is the most obvious. Interest rates go up, so taking out a loan for starting that new restaurant, building that new house, or financing that new municipal bridge is more expensive. In response, people delay those projects or never pursue them. All that economic activity is forgone.

Next, the wealth story is the most contestable. The interest rate change makes existing assets worth less. Let’s say you bought a stock last year guessing it would pay out $100 in dividends each year. At the same time, the bond you were considering buying was throwing off only $80 a year in coupon payments. Everyone recognizes the stock is giving a higher return (leaving aside risk for a moment). Now interest rates change, and the comparable bond is now throwing off $100 a year. Your stock will still give the same dividends, as the business model of the company should not have changed significantly. The stock is now worth less compared to the alternative bond, and its price should drop. Meaning, that a bunch of existing asset holders will get less wealthy. That much is clear. However, what is their propensity to start saving more in the face of that dip. Meanwhile, a bunch of debt holders should become more wealthy as their burden is inflated away? Does their propensity to spend more potentially out weight the asset holders new motivation to save. I have not researched the topic deeply, but it does not seem obvious that these wealth effects should be decisively contractionary.

Finally, the exchange rate should appreciate. The market for a country’s goods and assets has to clear at the same time, moving the price of the currency in complicated ways. In this case, a higher real interest rate should cause more investment to flow into the USA causing more people to buy dollars, driving up its price. In theory that appreciation will make imports cheaper and exports more expensive. Those cheaper imports lower the price level for Americans. Meanwhile, our exports have become less competitive, cooling demand for the American market. I say that this is all theory because most goods all over the world sold for export will be priced in dollars already. Thus, if you believe in sticky prices a move in the dollar might not affect their nominal price, in which case imports would have the same nominal price for Americans. Meanwhile, our exports have gotten more expensive but other countries’ exports are also priced in dollars and so have gone up just as much. Nevertheless, prices are not completely sticky, so the exchange rate effect is probably an important part of how rate hikes cool the economy.

Importantly, these three mechanisms are all financially mediated rather than direct. Matt Yglesias explains, the mechanical view “is that the impact of central banks on the economy is hydraulic. They do things (buying bonds, setting interest rates) that mechanically influence the economy by changing credit conditions. The other [correct] view is that central banks impact the economy primarily by coordinating expectations — they say things that lead to financial market reactions, which in turn influence the real economy.” More important than the rates set right now are how the financial markets expect the rates to move in the future based on the Fed’s statements. Long-term borrowing rates, the stock market, and the exchange rate are all more affected by the market’s expectation of future rates rather than what the Fed is setting right now. Which, brings us to the first explanation of why we were spared recession.

Credibility

Above I quoted Tyler Cowen arguing that credibility saved the day. People saw the Fed act, believed it would work, and set their prices accordingly to match the low inflation they now expected. Thereby, solving the problem. He was explaining how inflation slowed without the employment drooping. I will slightly spin this argument to explain why we have not seen a recession from the actions already taken. As financial markets saw inflation coming down, they began to expect that the high rates would not last for long. For reasons unclear to me, in October 2022 a new consensus began to emerge that the Fed would reverse course within the medium term, and today’s prices began adjusting accordingly. I think there was some good news on inflation around this time but nothing so dramatic as to be the obvious cause of this switch.

In the exchange rate, we can see that after a period of appreciating the dollar began depreciating last October:

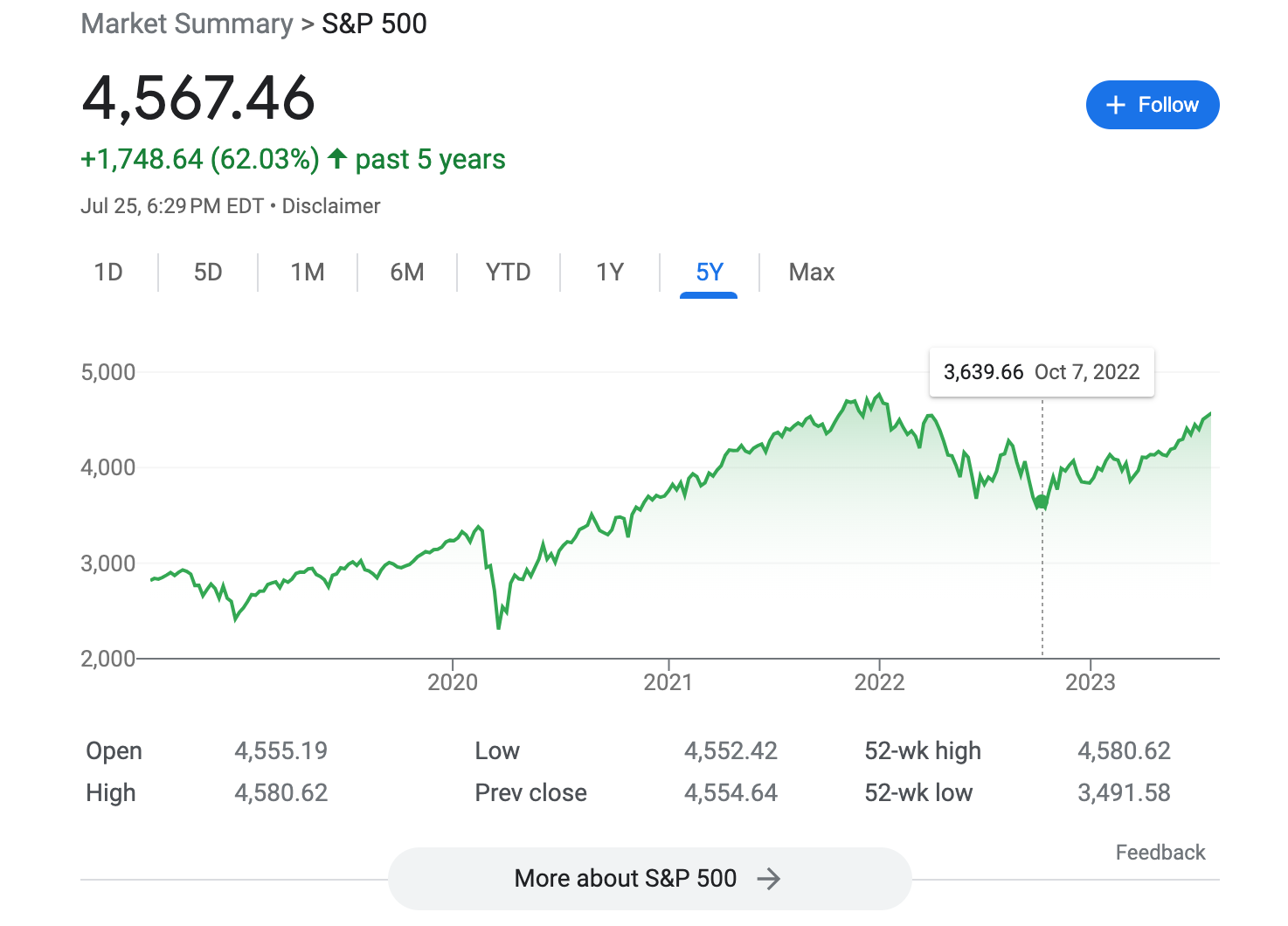

The S&P 500 also bottomed out in October:

Even, the growth in commercial interest rates began changing around this time:

On all three transmission mechanisms that we discussed above, contractionary conditions seem to have been easing or holding steadier since October.

I tried extending this analysis to residential construction. Dealing with physical projects rather than liquid asset markets will create some lags, but from this graph, you could argue that the October reassessment began slowing the drop in new home construction (though the case is less clear):

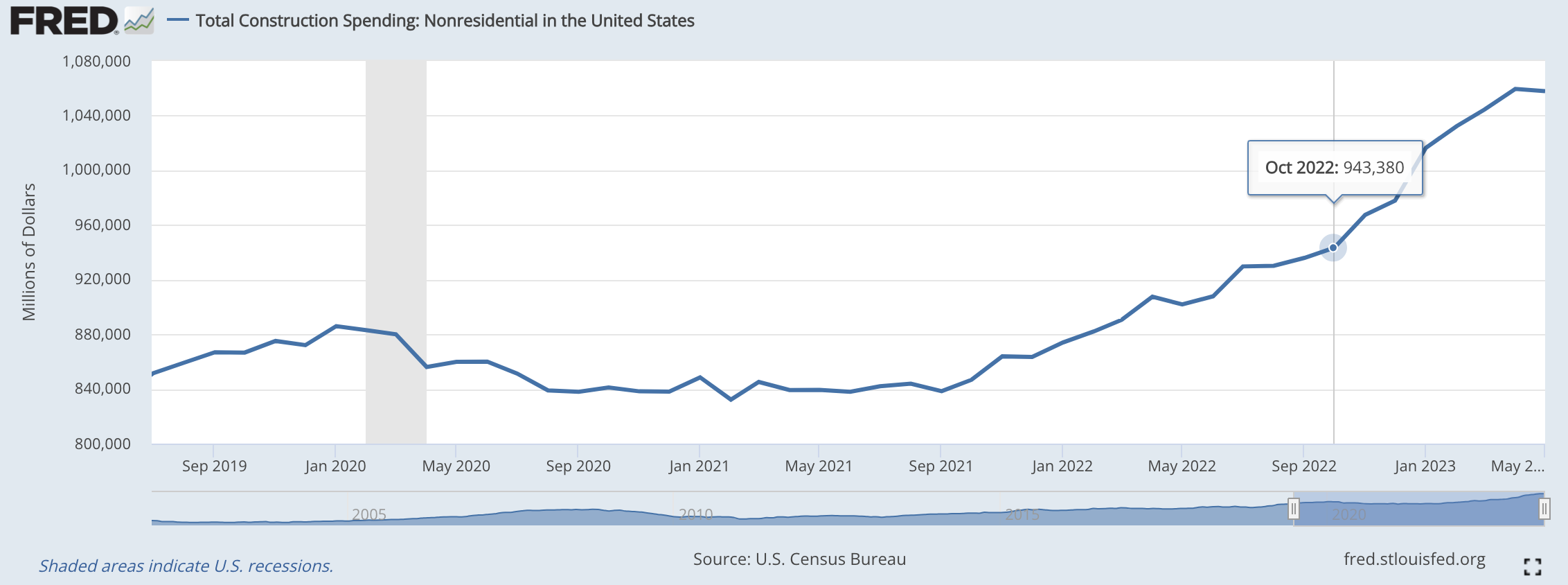

Further helping this situation, as Krugman has pointed out the decline in new residential construction has been offset by an increase in non-residential construction. He argued that this construction boom may have been caused by Biden’s infrastructure, semiconductor chips, and climate acts all of which subsidize domestic manufacturing. That seems a little on the nose to me. Especially, since this trend began in Fall 2021, and the infrastructure bill came at the tail end of that fall. The other bills were much later. If you squint at this graph, you can see construction picking up even faster after October 2022, but certainly, this trend was already going:

This record makes a strong case for the Fed’s actions. They were able to have their cake and eat it too. They continued raising rates to maintain their credibility, but financial markets saw inflation coming down and they were able to abate much of the contractionary impulse.

The Real Theories

Earlier, I introduced the idea of a “Real Theory” of recessions. In this telling, recessions come from managers reassessing their business models and closing down less productive divisions. However, what if those managers just cut unviable divisions and rethought their strategies two years ago?

COVID was the ultimate unwinding of the American labor market. If you had a part of your business with dim long-term prospects, you would have cut it just two years ago. Likewise, the low-hanging fruit of vulnerable businesses that would have gone under in this hypothetical recession likely never opened back up after COVID . Therefore, we should not expect much disruption this year, because the mega-disruption of the past three years already allowed the firms to change up their business models.

How can we test this theory? Well, countries varied in their COVID-response strategy: either supporting jobs or supporting workers who lost their jobs. In one strategy, you would step up unemployment insurance, encouraging separations but softening the blow. In another strategy, you would pay firms to keep workers on the rolls even if their functions no longer required (or allowed for) full-time work. I am sure to an extent all countries did both. However, we do see substantial differences between countries in the extant labor market churn. In America, the unemployment rate reached ~15%, whereas in Germany, which leaned more towards the protecting jobs approach, the unemployment rate only reached 6.4%. A “Real Theory” would predict that a higher unemployment rate during COVID would lessen the impetus to lay off workers now. I tried looking at this data but had trouble finding trustworthy cross-country comparisons of unemployment for right now. The European interest hikes began several months after ours, meaning that they are less likely to be out of the woods than we are. Also, the Russian invasion scrambling much of Europe’s energy model is obviously confounding. In a few months, I’ll look into testing this theory once with more timely data.

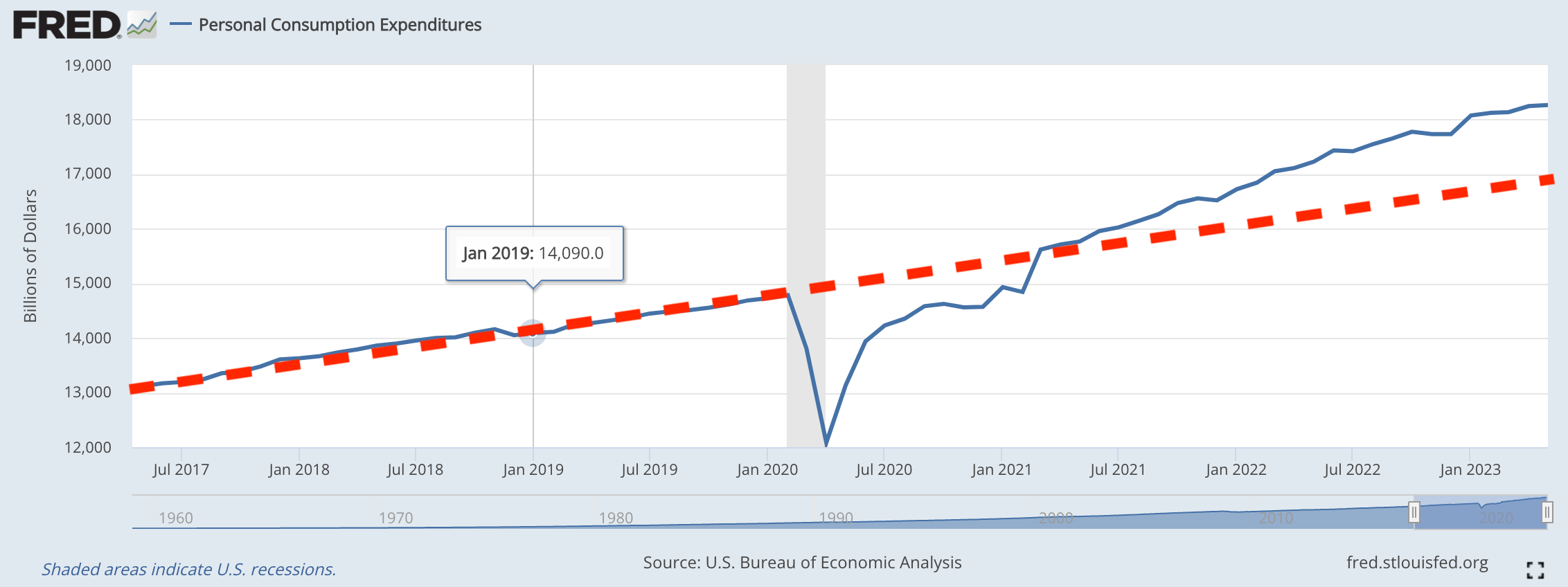

Savings Accumulated During COVID

This graph is pretty striking:

Consumption is very high and shows no signs of slowing. COVID prevented all kinds of spending, a hot stock market, and federal transfers paired with state tax cuts all meant that Americans built up significant savings during COVID. My first explanation would be that this extra consumption comes from households spending down that surplus. However, If anything we seem to be moving further from the trend line, rather than towards it.

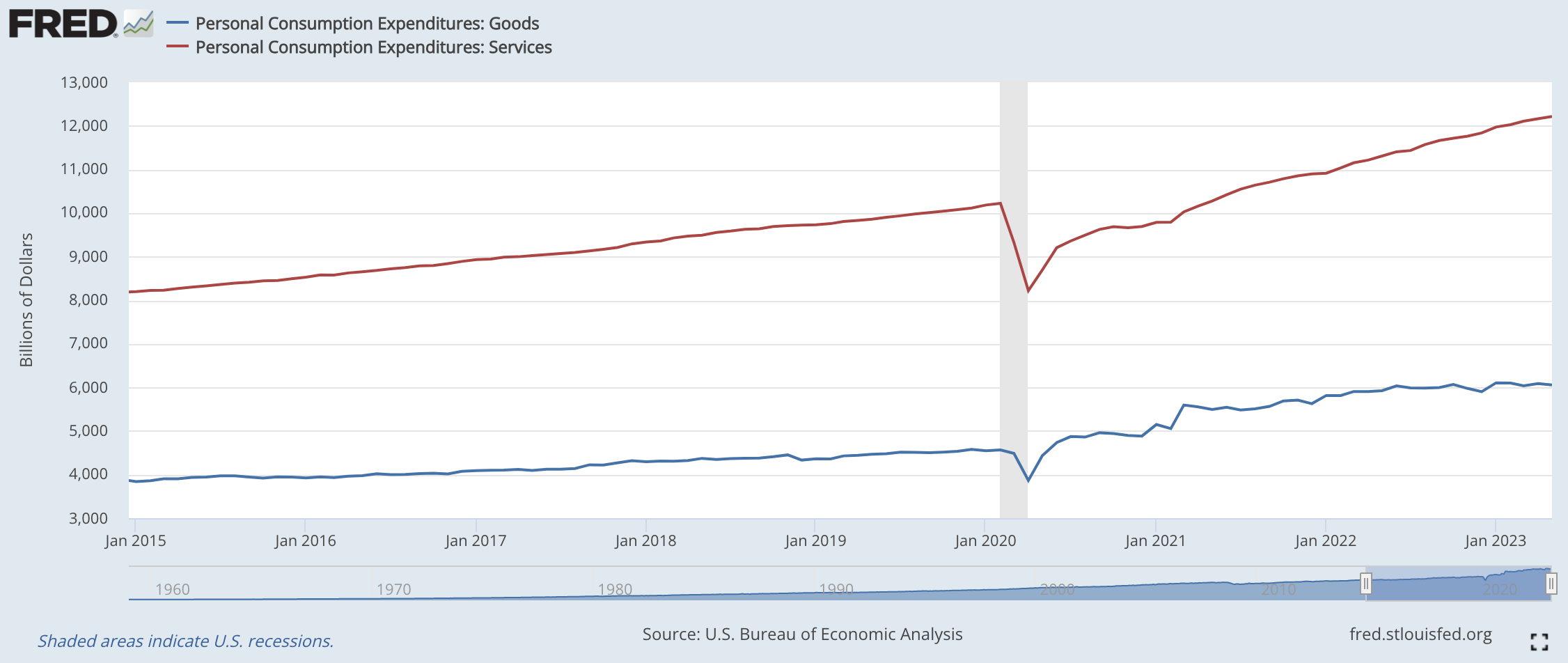

Perhaps habits were slow to change coming out of COVID, and only now have people regained the facility of eating out, going to concerts, or vacationing with the same abandon as they had before. It would take time for our demand for services to return, and now that they have people are spending down their COVID accumulations. Supporting this interpretation, the continued growth in consumption is coming more from services than it is from goods (which has been more or less flat for months).

Why Didn’t We Need A Recession?

The underlying assumption behind many of the recession predictions was that the labor market could not cool without a recession. How did we achieve this immaculate disinflation? Does it vindicate Team Transitory?

I think not. If all the trouble was coming from supply chains, we would expect a move in relative prices as certain items become unavailable and more expensive. Then, they would become available and prices should have returned to the ex-ante levels. Instead, what we have been left with is a permanently high price level. It affected many goods without supply chain issues and prices are not returning to their previous level. To be most charitable, perhaps the supply chain disruptions temporarily un-anchored inflation expectations, but once those initial problems stopped people’s expectations returned to our low-inflation norm. But, there were some other transitory stories that we could tell in addition to the supply chain story :

— The huge fiscal stimulus of the ARP came and went. Once, it went away that source of extra spending was gone. Thus, if you pin the blame on ARP, you should also expect any easier road out of the problem.

— Another factor was the mismatched services-to-goods ratio. Out of genuine social distancing or old COVID habits, in 2021 and 2022 people were consuming more goods and fewer services than they had before. That meant that goods producers might be stretched in their capacities, fielding more orders than normal. They were hesitant to expand production in response to a probably temporary pick up in business and raised prices instead. Meanwhile, service providers had more capacity and could absorb more demand without raising prices. Imagine a hotel that was at 40% capacity in 2021 but reached 80% capacity in 2023. In this scenario, they would now be serving more people but would not yet be at a point where they would need to raise their prices. Like the standard supply chain story, this factor alone would move relative prices not the price level. However, it could contribute to a temporary un-anchoring of inflation expectations. Furthermore, it means that the post-COVID consumption boom might support growth without being inflationary, if the new spending went to service providers not yet at capacity.

— Getting people back to work (we saw a steady rise in America’s workforce participation over the past two years) and reopening the borders to immigration should have cooled the labor market, all else being equal.

All these factors made inflation get out of control in 2021 but start coming down by the end of 2022. The Fed had credibly signaled that they were willing to act if need be, and markets began planning for lower rates in the near future. Together with firms that had just readjusted their models and consumers who were eager to spend, conditions might be right to pull off a…

I won’t jinx it by saying it.